IB Economics:

|

|

What is economics? – Topics:

|

|

WHAT is economics? Learning objectives

|

Economics is a social science:

The problem of choice: Explain that land, labour, capital and entrepreneurship are the factors of production

Essential economic questions:

|

|

The study of economicsEconomics is the social science that studies how people use scarce resources to satisfy unlimited needs and wants. You will notice it is a social science because it is about how people interact and why they behave in certain ways. In some respects it is a lot like psychology because we talk and make decisions based on our understandings of why people do what they do.

Social science, which includes economics, psychology, sociology, anthropology and political science, consists of the disciplined and systematic study of society and its institutions, and of how and why people behave as they do, both as individuals and in groups within society. The economics classroom! |

What is economics?

The world's resources are limited and already overstretched. Economics is the study of scarcity and decision-making.

|

Economics as a social scienceEconomics is the scientific study of the ownership, use, and exchange of scarce resources – often shortened to the science of scarcity.

Economics is regarded as a social science because it uses scientific methods to build theories that can help explain the behaviour of individuals, groups and organisations. Economics attempts to explain economic behaviour, which arises when scarce resources are exchanged. In terms of methodology, economists, like other social scientists, are not able to undertake controlled experiments in the way that chemists and biologists are. Hence, economists have to employ different methods, based primarily on observation and deduction and the construction of abstract models. As the social sciences have evolved over the last 100 years or so, they have become increasingly specialised. This is true for economics, as witnessed by the development of many different strands of investigation including microeconomics and macroeconomics, pure and applied economics, international economics, development economics and industrial and financial economics. What links them all is the attempt to understand how and why exchange takes place, and how exchange creates benefits and costs for the participants. |

What is social science?Social science: The scientific study of society – of human behaviour and of social interactions. Economics is one of several social sciences. Others are sociology, political science, and anthropology. Economics is considered a social science because it seeks to explain how society deals with the problem of scarcity.

Scarcity is the situation in which available resources, or factors of production, are finite, whereas wants are infinite. There are not enough resources to produce everything that we need and want. The basic economic problem that arises because people have unlimited wants but resources are limited. Because of scarcity, various economic decisions must be made to allocate resources efficiently. |

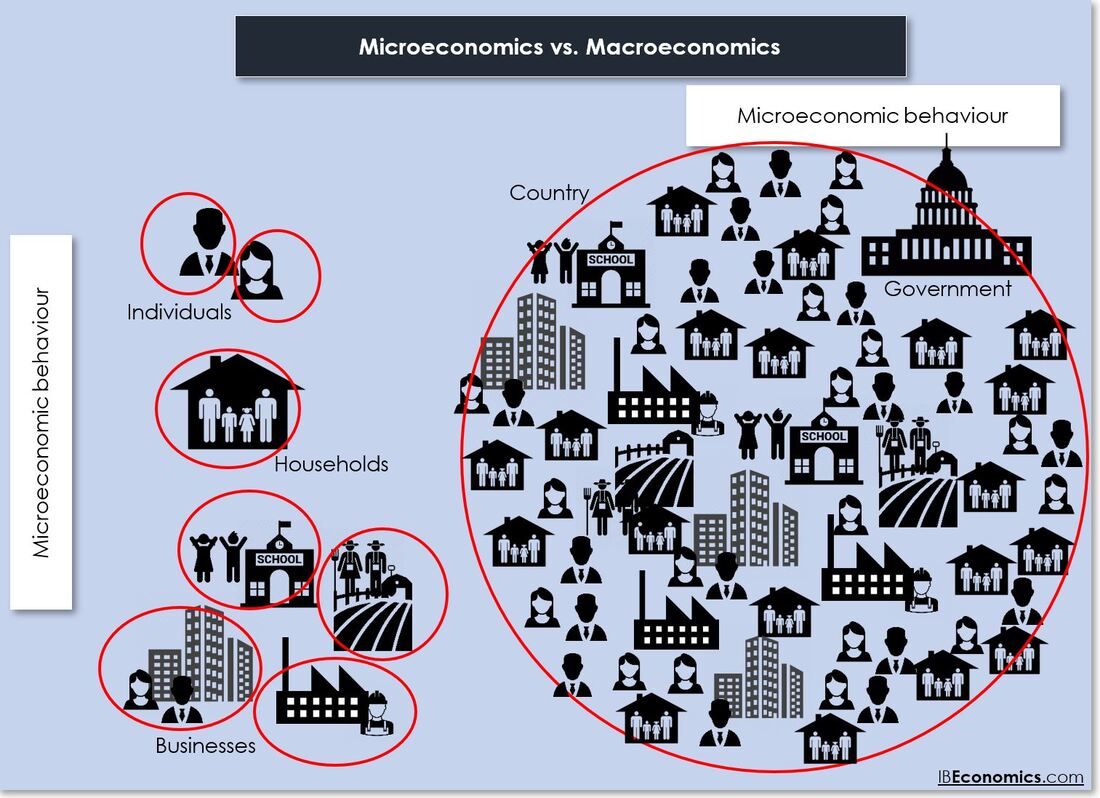

THe basis of economics: microeconomics and macroeconomics

What is microeconomics?Microeconomics analyses basic elements in the economy, including individual agents and markets, their interactions, and the outcomes of interactions. Individual agents may include, for example, households, firms, buyers, and sellers. For example, firms sell goods to households, and households provide labour.

|

WHAT IS MaCROECONOMICS?Macroeconomics analyses the economy as a system where production, consumption, saving, and investment interact, and factors affecting it: employment of the resources of labour, capital, and land, currency inflation, economic growth, and public policies that have impact on these elements.

MICRO vs MACRO ECONOMICS |

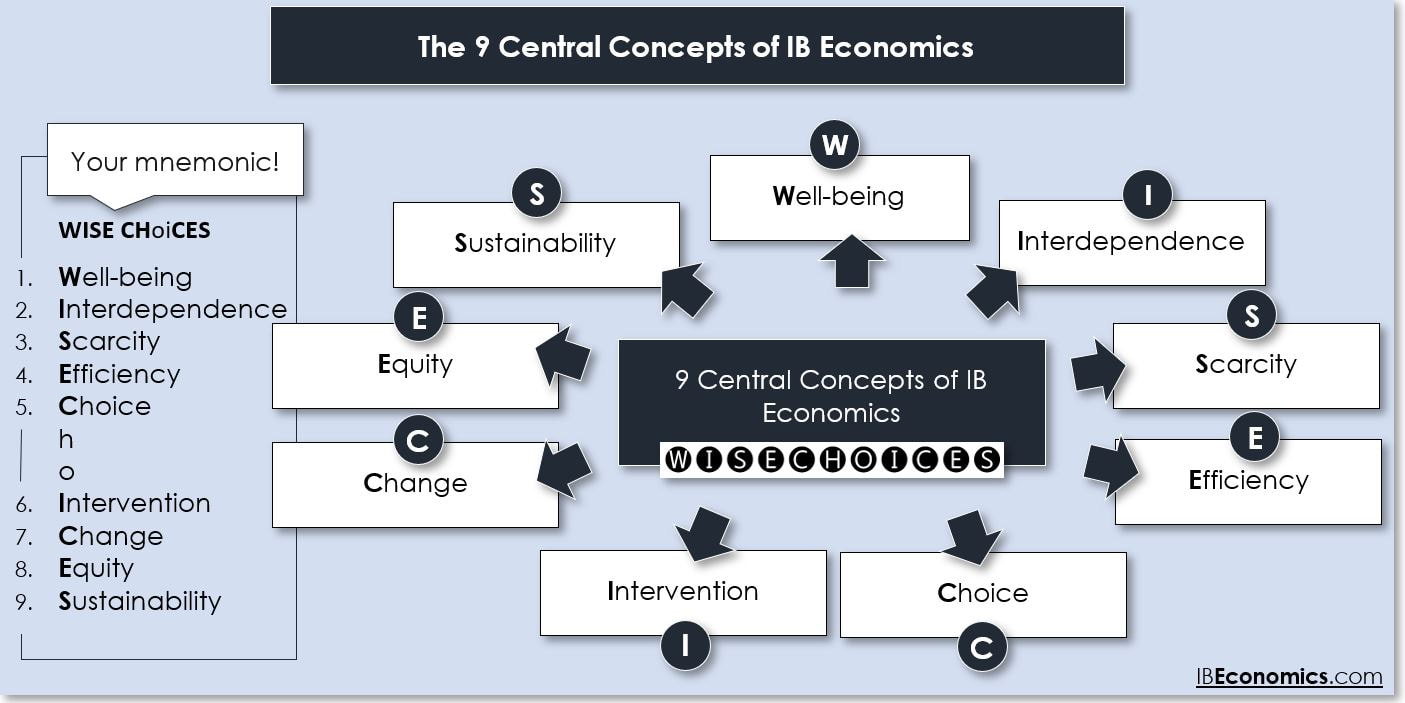

Central Concepts in Economics

Well-Being(Economic) well-being: Equality is not the same as equity. Equality refers to the same or similar economic outcomes for different groups or individuals. Equity relates to fairness, a normative concept. A normative statement is one that makes a value judgment. Such a judgment is the opinion of the speaker; no one can “prove” that the statement is or is not correct. Inequity (unfair) is often referred to as inequality, in economics, and may refer how income, wealth or even opportunity is distributed in society. Irrespective of society or economic system, inequity and inequality are significant issues, both between societies (e.g., Zimbabwe and Denmark) and within societies (e.g., men and women in Saudi Arabia). An area of economic debate is whether markets or governments can, or even should, create more equity and reduce inequality in societies.

ScarcityScarcity: Scarcity is a central concept in economics. Scarcity is the situation in which available resources, or factors of production, are finite, whereas wants are infinite. There are not enough resources to produce everything that we need and want. The basic economic problem that arises because people have unlimited wants but resources are limited. Because of scarcity, various economic decisions must be made to allocate resources efficiently.

ChoiceChoice: Economics is the study of choice because resources are scarce and many needs and wants cannot be satisfied. As such, choices must be made, and whenever a choice is made an opportunity arises. Households, businesses and governments are always making choices between alternatives competing with each other. The consequences of such choices, present and future, is studied in economics.

ChangeChange: Change is an essential concept in economics. As economists, we need to be aware that the economic world is in a state of constant change and adjust our thinking accordingly. Change is an important concept in economic theory and in empirical evidence from the real world. Change is relevant to economic variables (e.g., a change in the unemployment numbers) and from one situation to another (e.g., a Russian invasion of a sovereign nation). Our economic world is subject to profound and continuous economic change that occurs in technologies, institutions, and societies, as well as structural change (a dramatic shift in the way an industry or market functions).

SustainabilitySustainability: Sustainability focuses on meeting the needs of the present without compromising the ability of future generations to meet their needs. Sustainability refers to limits on current economic activities that harm our environment by depleting and degrading resources, negatively impacting future generations (e.g., climate change won’t impact boomers as severely as Gen Zs or Gen Alphas). Good economic analysis considers sustainability as our world’s resources, boundaries and capacities are pushed to their limits.

|

InterdependenceInterdependence: Individuals, communities and countries are interdependent, not self-sufficient. Economic groups such as consumers, households, businesses, and governments all interact together within and across national borders to achieve their economic goals. The more these groups interact, the more they are interdependent. The economic world is highly interdependent, and decisions made by economic actors can cause many unintended consequences for other economic actors. When conducting an economic analysis, it is important to consider interdependencies.

EfficiencyEfficiency: Efficiency is quantifiable – a ratio of inputs to outputs. Efficiency could be using less inputs to achieve the same quantity of output or using the same amount of inputs to achieve greater output. Allocative efficiency is where scarce resources are put to their best possible use in producing goods and services in optimal combinations for society, minimising the waste of resources.

InterventionIntervention: In economics, intervention means governments getting involved to rectify perceived failure in markets (e.g., taxation and redistribution). Markets may be the most efficient at organising scarce resources, but they often fail to achieve many of the goals of societies such as economic well-being, equity, or sustainability. Such failures may be considered just cause for government intervention, however, there is considerable disagreement between policy makers and economists as to the need for intervention, the type of intervention to be used, and the extent of any such intervention. There is much debate about the merits of the free market and the merits of intervention.

EquityEquity: Equity, being different to equality (sameness), refers to the normative concept of fairness. Fairness has a different meaning from one person to the next. Inequity (unfair) is often referred to as inequality, in economics, and may refer how income, wealth or even opportunity is distributed in society. Irrespective of society or economic system, inequity and inequality are significant issues, both between societies (e.g., Zimbabwe and Denmark) and within societies (e.g., men and women in Saudi Arabia). An area of economic debate is whether markets or governments can, or even should, create more equity and inequality in societies.

|

SCARCITY – FACTORS OF PRODUCTION ARE FINITE AND WANTS INFINITE

|

Needs, wants and resources.

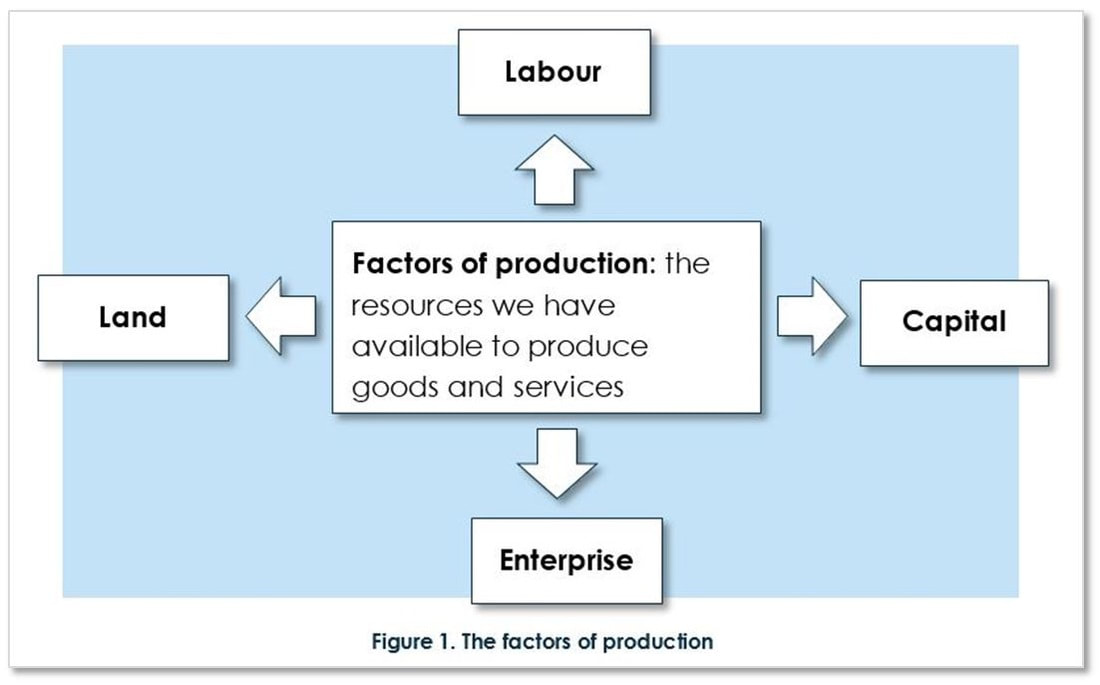

Our needs and wants are very different. We need some things just to stay alive – including water, food and warmth. But our wants are never-ending (infinite). We may want a PlayStation 4 for Christmas. Do we actually need it to stay alive? Most people would say no – it is simply a luxury that would be nice to have. Imagine you get a PlayStation for Christmas – what will you want for your birthday? An iPhone, perhaps. The cycle of wants continues, once you get one thing, you move straight on to wanting another. In contrast, the resources used to produce these goods and services are in limited supply (finite). Collectively, resources are called factors of production. Resources can be divided into four groups:

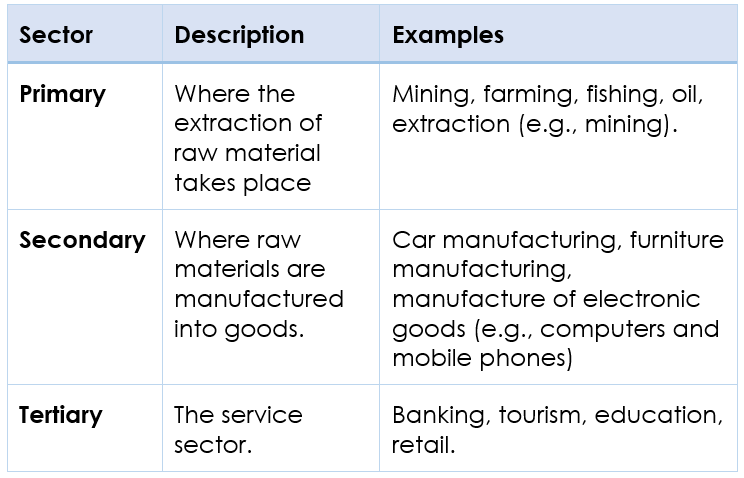

Production of goods and services. Goods are items that you can touch (tangible) – you can take them home and use them. An example of a good is a pen or a packet of crisps. A service is something that someone provides for you; you cannot touch it (intangible). Examples include tourism and banking. The production of nearly all goods and services uses up scarce resources. Production takes place in one of three sectors, as shown in the table.

|

Factors of production

|

ChoicesThe basic economic problem: as a result of scarcity choices must be made. The basic economic problem occurs because resources are scarce – but our wants are infinite. As resources are scarce and our wants are never-ending, we have to allocate resources. When we allocate resources, we ask the following questions:

When allocating resources, individuals, firms and governments must all make decisions about what, how, and for whom. |

Scarcity and choice

|

EVERY ECONOMIC CHOICE HAS AN ASSOCIATED OPPORTUNITY COST

|

Opportunity costs and choices.

We already know that resources are scarce and we have infinite wants. This creates a problem; if we cannot have everything we want, we have to make choices. I really want to go on holiday and I would like a new car. I do not have the money to do both, so I must decide which I would like to do the most. If I choose to go on holiday, it means I cannot buy a new car. I can therefore say that the opportunity cost of going on holiday is buying a car. This means that when I have chosen the holiday, the next best alternative is the car. Thus, because we cannot have everything we want as a result of scarcity, every choice that must be made between two or more options has an opportunity cost. Free goodsA free good is a good that is not scarce, and therefore is available without limit. A free good is available in as great a quantity as desired with zero opportunity cost to society. A good that is made available at zero price is not necessarily a free good.

Examples of free goods:

|

Opportunity cost – the next best alternative foregone when making a choice – what we give up when we make a choice.

|

ECONOMIC QUESTIONS THAT MUST BE ANSWERED BY ANY ECONOMIC SYSTEM

|

Scarcity makes every economy in the world, regardless of how it is organised, to answer three basic questions – What to produce? How to produce? For whom to produce? The first two questions are about resource allocation.

Resource allocation refers to assigning an economy’s available resources, i.e., the factors of production, to certain uses which have to be chosen among the many possible alternatives available. For example, if ‘a what to produce?’ choice involves choosing a certain amount of education services (schools, universities, etc.) and a certain amount of health care (medical centres, hospitals, etc.), this means a decision is made to allocate some resources to the production of education and some to the production of health services. At the same time, a choice needs to be made about how to produce these services. Which factors of production (e.g., labour – doctors, nurses, dentists, teachers, professors, and capital – buildings, information systems, equipment) and in what quantities (for example, how much labour, how much capital equipment and what type of capital equipment, etc.) should be used to deliver health care and how much to deliver education services. Bearing in mind that resources are scare relative to needs and wants, if a decision is made to change the amounts of services produced, such as more education and less health care, this involves a reallocation of resources. Sometimes, economies do not produce the best amount of goods and services relative to what is socially desirable. For example, if too many cigarettes or alcohol are being produced, then there is an overallocation of resources in production of cigarettes or alcohol. If too few socially desirable goods or services are being produced, such as health care or education, then there is an underallocation of resources in producing these services.

|

The third and final question, ‘for whom to produce’ is about the distribution of output, i.e., how much output different individuals or different groups in the economy receive.

Here the distribution of income among individuals and groups in an economy becomes an important consideration. To a large extent the amount of output different people receive depends on how much of it they can buy, which is dependent on how much income they receive. When the distribution of income or output changes so that different social groups now receive more, or less, income and output than previously (e.g., taxing the rich to provide education for the poor), this is referred to as redistribution of income. WEALTH AND INCOME DISTRIBUTIONIncome inequality in the UK |

ECONOMICS EXAMINES HOW RESOURCES ARE ALLOCATED

|

The economic problem – sometimes called the basic, central, or fundamental economic problem – is one of the fundamental economic theoretical principles in the operation of any economy. It states that there is scarcity; that is, that the finite resources available are insufficient to satisfy all human wants and needs. The question then becomes how to determine what is to be produced, and how the factors of production (such as capital and labour) are to be allocated. Economics revolves around methods and possibilities of solving this fundamental economic problem.

The economic problem can be divided into different parts: 1. Problem of allocation of resources The problem of allocation of resources arises due to the scarcity of resources, and refers to the question of which wants should be satisfied and which should be left unsatisfied; in other words, what to produce and how much to produce. More production of a good implies more resources required for the production of that good, and resources are scarce. These two facts together mean that, if a society decides to increase production of some good, it has to withdraw some resources from the production of other goods; in other words, more production of a desired commodity can be made possible only by reducing the quantity of resources used in the production of other goods. The problem of allocation deals with the question of whether to produce capital goods or consumer goods. If the community decides to produce capital goods, resources will have to be withdrawn from the production of consumer goods. However, in the long run, the investment on capital goods will increase the ability to produce consumer goods. Thus, both capital and consumer goods are important. The problem is determining what the optimal ratio of production between the two types of goods is.it is a social science that studies human behaviour as a relationship between end and scarce means that have alternative uses. 2. The problem of economic efficiency Resources are scarce and it is important to use them as efficiently as possible. Thus, it is essential to know if the production and distribution of national product made by an economy is maximally efficient. The production becomes efficient only if the productive resources are used in such a way that any reallocation does not produce more of one good without reducing the output of any other good; in other words, ‘efficient distribution’ means that any redistribution of goods cannot make anyone better off without making someone else worse off. The inefficiencies of production and distribution exist in all types of economies. The welfare of the people can be increased if these inefficiencies are ruled out. |

3. The problem of full-employment of resources

In view of the scarce resources, the question of whether all available resources are being fully employed is an important one. An economy should achieve maximum satisfaction by using the scarce resources in the best possible manner; resources should not be wasted or used inefficiently. However, in capitalist economies, the available resources are not fully employed. In times of recession, there are many people willing and wanting to work who go without employment. It supposes that the scarce resources are not fully being used in a capitalist economy. 4. The problem of economic growth If the productive capacity of the economy grows, it will be able to produce progressively more goods, which will result in a rise in the standard of living of the people in that economy. The increase in productive capacity of an economy is called economic growth. There are various factors affecting economic growth including the allocation of resources to capital goods, investment in technology and skills and education training to raise the productivity of labour. This part of economic problem is studied in the economies of development. ECONOMIC GROWTH |

ECONOMIC SYSTEMSThe existence of scarcity creates the basic economic problem faced by every society, rich or poor: how to make the best use of limited productive resources to satisfy human needs and wants.

To solve this basic problem, every society must answer these three basic questions:

Economic Goals and Societal Values. Societies or communities answer the economic questions in different ways. Societies look at economic goals and make decisions based on what is most valued. Some economic goals that are considered are:

|

TYPES OF ECONOMIC SYSTEMSEconomic Systems. An economic system is the method used by a society to produce and distribute goods and services. Several fundamental types of economic systems exist to answer the three questions of what, how, and for whom to produce: traditional, command, market, and mixed.

Traditional Economies: In a traditional economy, economic decisions are based on custom and historical precedent. For example, in tribal cultures or in cultures characterized by a caste system, people in particular social strata or holding certain positions often perform the same type of work as their parents and grandparents, regardless of ability or potential. Command Economies: In a command economy, governmental planning groups make the basic economic decisions. They determine such things as which goods and services to produce, their prices, and wage rates. Cuba and North Korea are examples of command economies. Market Economies: In a market economy, economic decisions are guided by the changes in prices that occur as individual buyers and sellers interact in the market place. As such, this type of economy is often referred to as a price system. Other names for the market system are free enterprise, capitalism, and laissez-faire. The economies of the United States, Singapore, and Japan are identified as market economies since prices play a significant role in guiding economic activity. Mixed Economies: There are no pure command or market economies. To some degree, all modern economies exhibit characteristics of both systems and are, therefore, often referred to as mixed economies. For example, in the United States the government makes many important economic decisions, even though the price system is still predominant. Even in strict command economies, private individuals frequently engage in market activities, particularly in small towns and villages. The key point to remember is that every individual and every society must contend with the problem of scarcity. Every society, regardless of its political structure, must develop an economic system to determine how to use its limited productive resources to answer the three basic economic questions of what, how, and for whom to produce. Under capitalism, man exploits man. Under communism, it's just the opposite. |

Market vs government

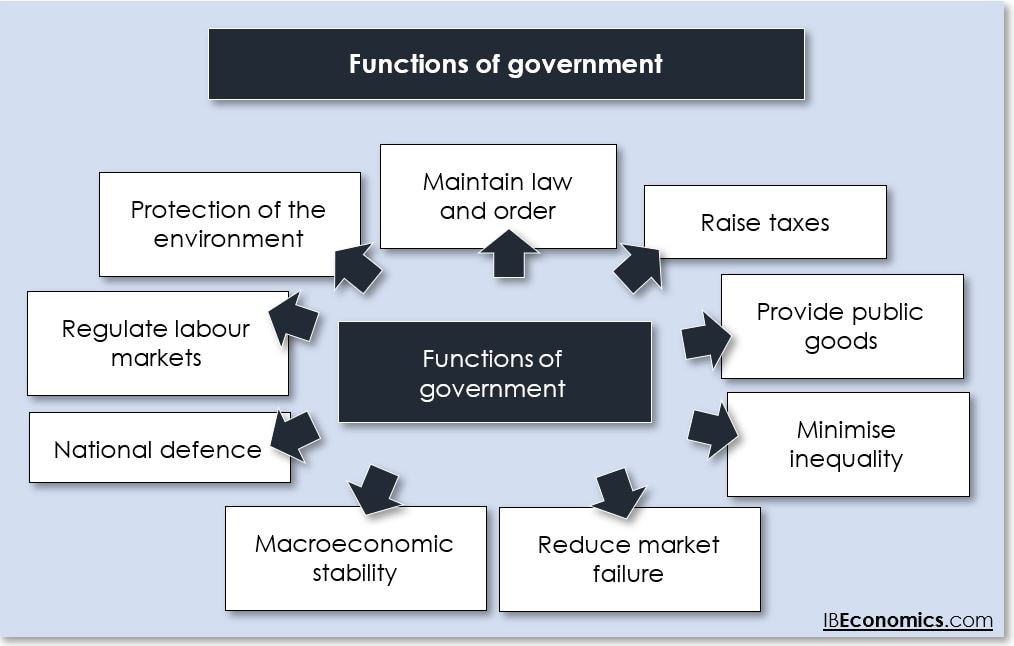

Market versus government intervention. One of the main issues in economics is the extent to which the government should intervene in the economy. Free market economists argue that government intervention should be strictly limited as government intervention tends to cause an inefficient allocation of resources. However, others argue there is a strong case for government intervention in different fields, such as externalities (e.g., pollution caused by factories), public goods (e.g., policing and firefighting) and monopoly power (e.g., pharmaceutical companies that can set their own prices for crucial drugs).

Arguments for government intervention:

Arguments against government intervention:

|

Markets can be efficientMarkets need governmentMarkets and government

|

|

|

|

|

IB Economics 1.1 What is economics?

Summary Notes

IB Economics: 1.1 What is economics? teaching and learning PowerPoint notes for HL and SL IB Economics.

PROGRESS CHECK - TEST YOUR UNDERSTANDING BY COMPLETING THE ACTIVITIES BELOW

You have below, a range of practice activities, flash cards, exam practice questions and an online interactive self test to ensure you have complete mastery of the IB Economics requirements for the Introduction to Economics: What is economics? topic.

USE THE FLASHCARDS IN ALL THREE STUDY MODES

IB Economics 1.1 What is economics?

|

IB Economics 1.1 What is economics?

|

|

|

IB Economics interactive QUIZZES AND TWO CLASSROOM GAMES

Test how well you know the IB Economics Introduction to Economics: What is economics? topic with the interactive self-assessment quizzes below. Each interactive quiz selects 30 questions at random from a much larger question bank so keep on practicing! Aim for a score of at least 80 per cent.

|

Loading What is economics? A

|

Loading What is economics? B

|